Key Takeaways

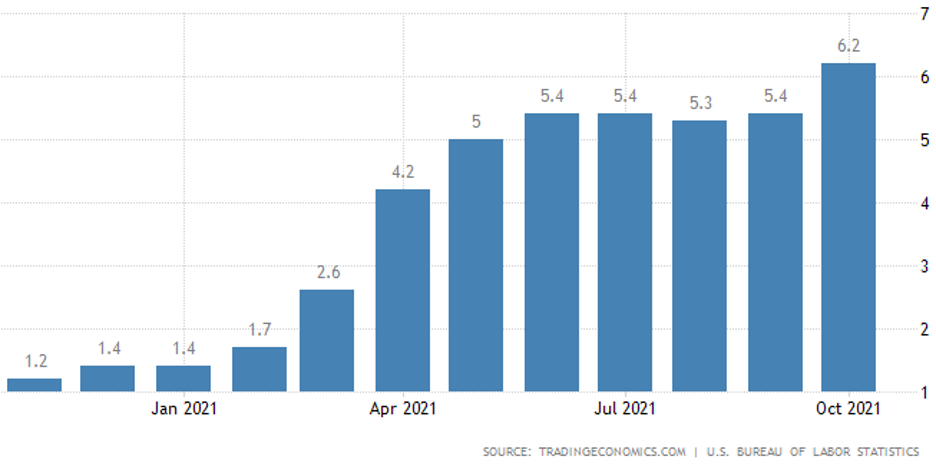

- Inflation in October 2021 was 6.2%, the highest in nearly 30-years.

- From 1914 to 2021, average inflation in the U.S. has been around 3.2% and the average return of the market (i.e., S&P 500) has been around 10-11%.

- While not without risks, investing in equities is a tested long-term hedge against inflation.

If you have been paying any attention to the news lately, whether financial or otherwise, you have likely heard about inflation. Going back to May, the annual inflation rate each month in the United States has been 5% or higher. In October, experts forecasted the inflation rate would be around 5.8%, but even that high estimate was lower than the 6.2% we saw instead. For financial historians, 6.2% is the highest inflation rate since November 1990.

The experts initially predicted that these higher inflation numbers were transitory, and we would get back to “normal” numbers in relatively short order. While they may still be correct, it is starting to look more and more like high inflation may be here to stay for a while. There are many reasons why inflation is surging as much as it is (COVID restrictions, supply chain bottlenecks, government spending, etc.) that it is hard for even the daily practitioner to make accurate predictions. Rather than get into the reasons for current inflation, let us instead delve into what you can do about inflation in terms of your own financial picture.

Oftentimes, we will talk with clients who are apprehensive about investing in the market for any number of reasons. The most obvious of which is that they do not want to see their account balances go down when the market goes down. However, the price you would pay for assurance against market downcycles is the probability that your funds will lose purchasing power to inflation.

Among our core investment philosophy is the idea that equities provide a good long-term hedge against inflation. For example, while inflation in recent months has been higher, Looking back from 1914 to 2021 the average inflation rate in the United States has been around 3.2%. During the same time, the average return of the market (i.e., the S&P 500 index) has been around 10-11%. This means that the average “real” return, meaning market return minus inflation, has been around 7%.

Disciplined portfolio management and appropriate diversification allows for good outcomes in a variety of economic scenarios. As you would imagine, we want our clients to own a fair amount of U.S. equities, but we also want them to own equities in foreign countries, both developed and emerging, for the years in which those outpace U.S. equities. For current or soon-to-be retirees who need access to living income in short order, we want them to own bonds, cash, and cash equivalents that are intended to hold their value against short-term market downturns. However, knowing that many retirees will need to live on their nest egg for thirty, forty, or fifty years, we also want them to own equities to provide growth that is intended to outpace longer-term inflation.

When we create financial plans for our clients, we routinely test them against high inflation, low market returns, and long life. The best thing our clients can do is keep us abreast of their spending needs and retirement timeline so we can be sure to have the necessary cash and bond investments that allows for disciplined investment on the equity side. Our job is to help create the finely tuned balance that optimizes our clients’ portfolios for any number of potential scenarios.

This is what we do for our clients. Give us a call if you are ready to have a conversation.

Sources:

Bureau of Labor Statistics; Consumer Price Index – October 2021; U.S. Department of Labor, November 10, 2021; https://www.bls.gov/news.release/cpi.toc.htm

CPI Inflation Calc; $100 in 1914; https://www.officialdata.org/us/inflation/1914?amount=100

S&P 500 Data; S&P 500: $100 in 1914; https://www.officialdata.org/us/stocks/s-p-500/1914

Trading Economics; United States Inflation Rate; https://tradingeconomics.com/united-states/inflation-cpi