What a difference a couple of years makes. Even the casual fan has likely heard the talk about interest rates and felt inflation during these past twenty-four months. Two years ago, in February 2021, the Federal Funds target rate was 0 – 0.25%. It remained there until just over a year ago in March 2022. Fast forward to today and we have seen eight rate hikes up to a current Federal Funds target rate of 4.5 – 4.75%.

For many, the Federal Funds rate is a number heard talked about in the financial news but are unsure how it affects their actual day-to-day lives. Quick example: in February 2021, both the 15- and 30-year fixed mortgage rates were under 3%. Today, both are above 6%.

Why is the Fed raising rates like this?

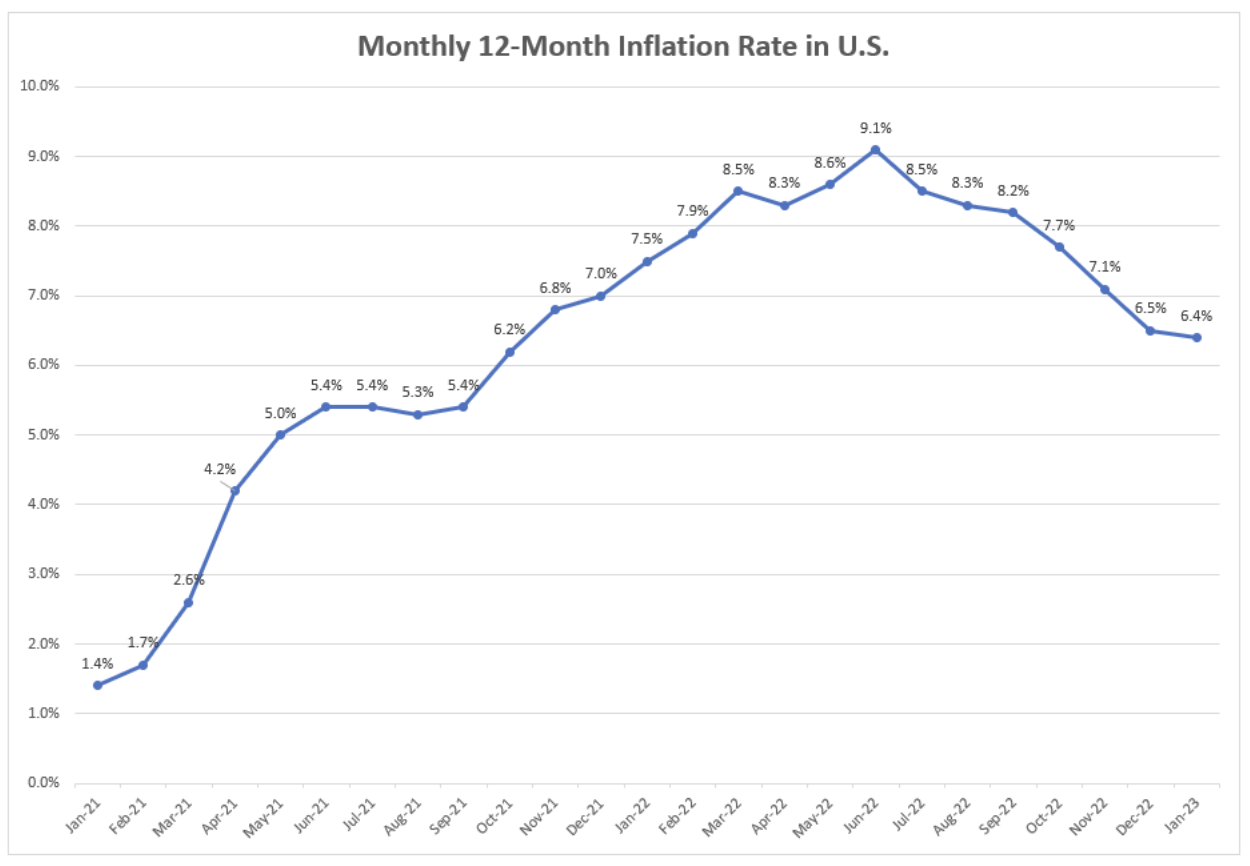

The Fed has a dual mandate: maximum employment and price stability. When unemployment is high, the Fed will lower rates to spur economic growth and increase jobs. When prices are unstable (i.e., when inflation is high), the Fed raises rates to slow the economy, tamp down on demand, and bring prices down. Because unemployment is currently still relatively low (3.4% in January 2023), the Fed feels that it can continue to increase rates, and because inflation is still relatively high (6.4% in January), the Fed feels that it needs to increase rates.

What we are seeing now, however, is that inflation appears to have peaked and is coming down, so the Fed’s feeling of needing to increase rates is moderating.

The Fed’s next meeting is in March, where the consensus expectation is that they will raise rates another quarter point. Before their most recent meeting, the Fed had been raising rates by a half to three-quarters of a percent at a time, so a quarter-point raise would be a welcome dose of moderation.

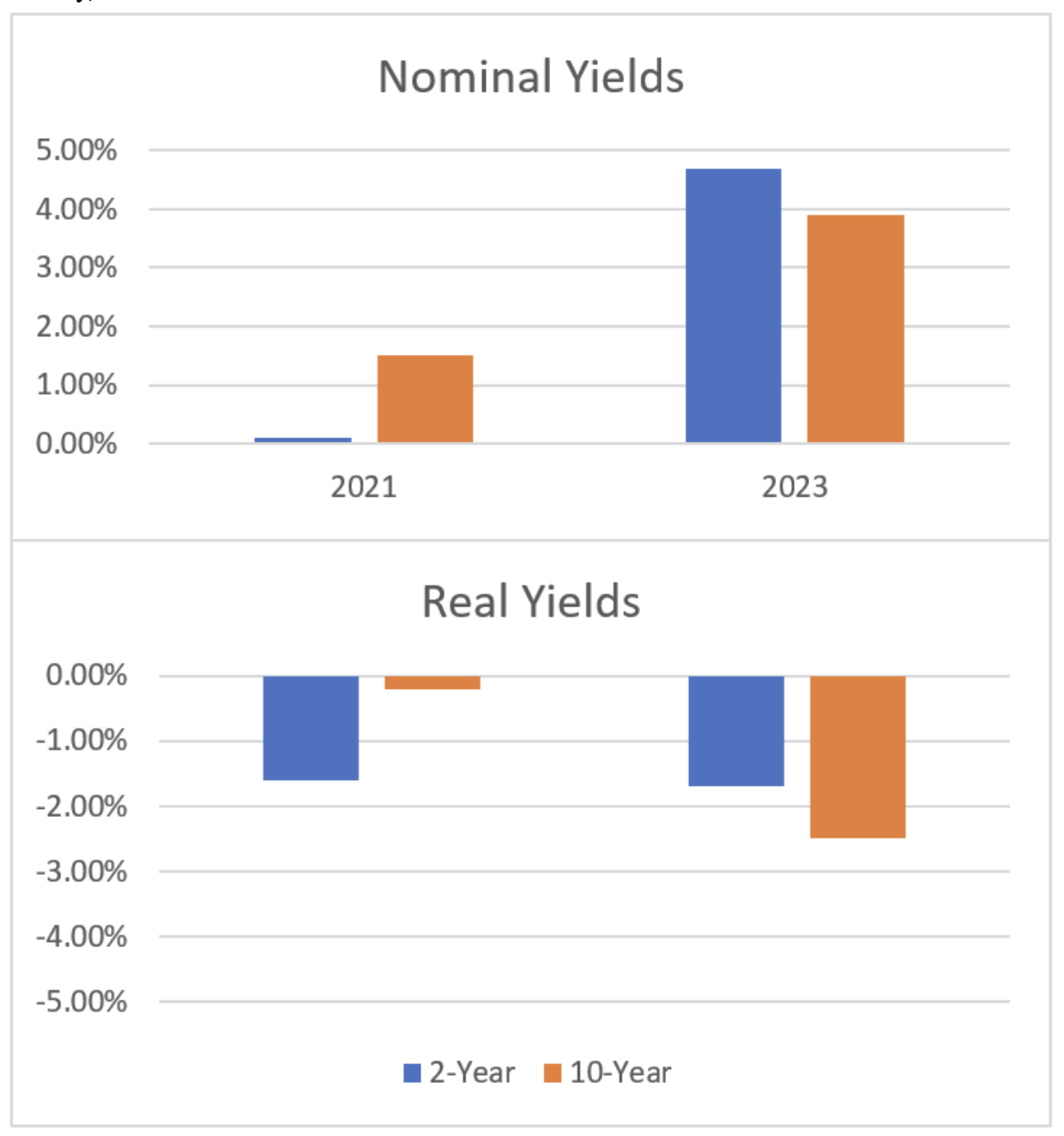

Amid all this focus on inflation and the Fed rate is an interesting tidbit. As the Fed has increased rates, so too have the yields on a fixed income. Looking back again to February 2021, 10-year treasury nominal yields were around 1.5%, and the two-year yield was around 0.1%. Today, the 10-year nominal yield is around 3.9%, and the two-year is around 4.7%. At a glance, this is a welcome change for fixed-income investors: finally, there is yield to be had!

However, times being as interesting as they are, we need to keep in mind the concept of real return or real yield, which is the excess of nominal return over inflation. Back in February 2021, inflation was 1.7%. Most recently in January, inflation is now at 6.4%. While nominal yields have increased, real yields today are actually lower than they were in 2021.

This anomaly will not last forever. As inflation continues to come down from its highs, real returns will increase accordingly. Ultimately, the Fed’s goal is to engineer a “soft landing” – they want to raise rates at a pace that will bring the economy, and inflation, to a gentle slowdown rather than a screeching halt. Time will tell whether they will achieve that goal. In the meantime, we will continue to monitor all the data and search for the best places to find yield for our clients.