Key Takeaways:

- Roth conversions should be especially considered if retired and not yet 70 years old.

- Withdrawing pre-tax funds and paying taxes before Social Security and Required Minimum Distributions (RMD) may result in less tax paid on those funds over the long term.

- Careful retirement income tax planning prior to age 70 may present significant long-term benefits for multiple generations.

Retiring before age 70 is the norm in the United States. While longevity continues to increase, the desire to retire later, work part-time in retirement or have a transitional job before retirement does not appeal to the masses. From a financial advisor standpoint, this presents ample financial planning opportunities for retirees before they reach age 70. Implementing these strategies, while meeting income desires may present long-term benefits that can even be passed on to the next generation. Simply saying, “I’m going to withdraw 4% from my account” or “I’m going to pay the least amount of taxes each year” can result in many missed opportunities.

One of our favorite planning techniques for a retiree who is pre-Required Minimum Distribution (RMD) age is to consider intentionally withdrawing funds from an IRA through annual Roth conversions.

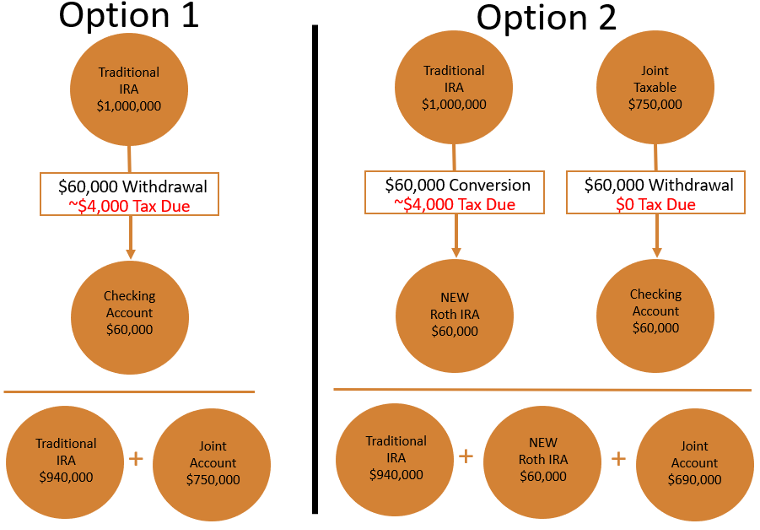

While there are multiple arguments for this approach, the most significant consideration is from a tax perspective. Consider a 62-year-old retiree couple who has $1,000,000 in IRA assets and $750,000 in a taxable account with a $500,000 basis. What would many retirees do to take income? Simple, take the withdrawal from the taxable account until the RMD and Social Security kick in and delay the larger tax bill until later.

While this is not terrible planning, we believe there is an alternative plan that should be considered.

We believe that taking partial withdrawals from the IRA prior to age 70 can help ultimately get the money out of the IRA at a lower tax rate. This is because early retirees have low taxable income before RMDs start and delayed Social Security income kicks in at the same time. Because we know these taxable income sources may start at age 70, we believe taking a part of the funds out of the IRA prior to age 70 can help reallocate taxable income into more income-tax-friendly years.

If you believe this is logical, we want to go one step further.

Instead of simply taking the IRA distribution out to pay for current expenses, we would advise considering a partial conversion of the Traditional IRA funds to a Roth IRA followed by a distribution from the taxable account for living expenses.

This would ultimately result in:

- the desired shifting of taxable income to the current year

- living expenses provided from the investment portfolio and

- a newly established Roth IRA replacing funds that would have otherwise been in a taxable account, subject to capital gains and dividend tax in higher-income years.

To help explain this, consider the previous example. The same couple with $1,000,000 in IRA money and $750,000 in taxable money needs $60,000 in income. In this case, converting the Traditional IRA to a Roth IRA for $60,000 and taking the $60,000 out of the taxable account for expenses results in a similar tax bill as withdrawing the funds from the IRA.

This is because capital gains tax on the distribution of the taxable money is phased in, and their income thresholds would make the capital gains tax rate 0%. See the chart below.

The result of this is removing the IRA funds at a low Federal income tax rate and potentially 0% State tax, depending on the state in which you reside. Additionally, all the growth in the newly created Roth IRA should be tax-free, while it may have otherwise been taxed at dividend and capital gains tax rates in the future*.

This strategy is very dependent upon the makeup of the client accounts, the income need, and the individual’s perspective on income taxes now and in the future. This is not a one size fits all approach and not all input factors are discussed in this commentary. If you feel this could benefit your situation or you would like to discuss it further, please do not hesitate to contact our office.

*Tax-free treatment of Roth IRA growth is subject to a five-year vesting period after the initial Roth IRA contribution.