Key Takeaways:

- Pass-through entity owners can choose to take profits as wages or distributions

- Increasing owner salary raises payroll tax liability but also increases future Social Security benefits

- Older owners and owners with non-working spouses and/or incomplete earnings records stand to benefit the most from increasing their salaries

Lower taxes are better, right? We spend a great deal of time planning around the tax code to help people accomplish their goals in the most tax-efficient manner. However, lowering taxes today often has consequences down the road. Sometimes there is a clear mathematical break-even, and other times a complex web of behavioral finance and unpredictable tax reform consequences make the picture murky. The latter is the case when it comes to business owners’ salaries.

Business owners have many more responsibilities than employees, but they also have a unique set of opportunities. One is the ability to set their wages. Owners of pass-through entities like S-corporations can choose to allocate their business profits between their salary and profit distributions. The most common line of thought we hear regarding this decision is to keep the owner’s salary low to avoid payroll tax, therefore shifting profits to owner distributions. One unintended consequence of this attempt to reduce tax in the current year is a potentially lower Social Security benefit in the future. Today we’ll think through the basics of this trade-off and search for best practices.

We’ll begin by stating the obvious: owners who work in the business can’t take zero salaries. The IRS says they must receive “reasonable compensation” and alludes to average salaries for similar services. If an owner of a company that nets $1 Million a year pays themselves $10,000, this is a red flag for audit and adjustment by the IRS. Once we get into this reasonable realm, there is a simple trade-off on each dollar of additional salary- the owner pays 15.3%¹ payroll tax on each dollar that could have otherwise avoided these taxes as an owner distribution.

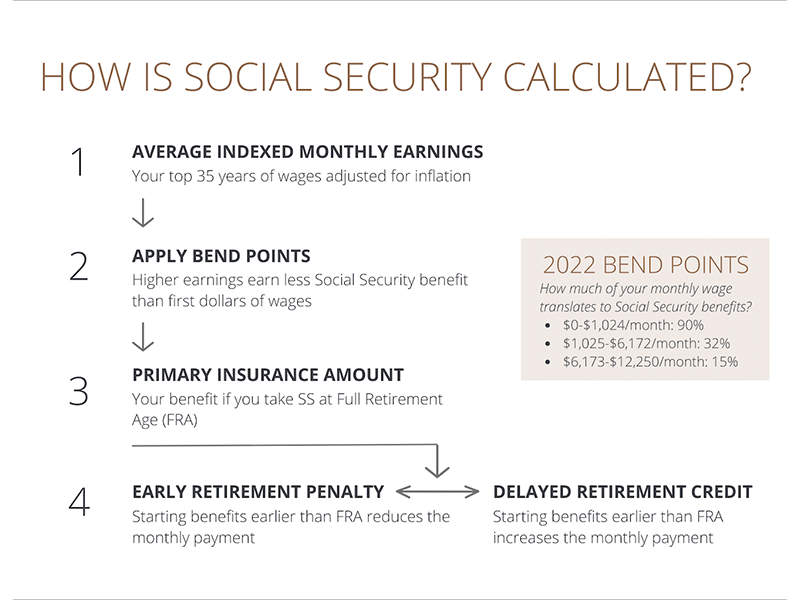

But how simple is this trade-off? Sure, it is easy to calculate the tax burden of an owner’s salary, but the Social Security calculation is very complicated. Your monthly benefit is determined by a four-step calculation in which each year, a salary figure is added to your earnings record. After 35 years, higher-earning years (adjusted for inflation) replace lower years. This means the marginal benefit of paying yourself an increased salary is very much tied to your previous work history.

How is Social Security Calculated?

Let’s examine how this works with a hypothetical. Jim, age 66, began his career as an electrician earning a competitive salary for 15 years. As his expertise grew, he decided to start his own business, sometimes earning minimal profit as the business grew. Now he manages several employees and the business netted $400,000 last year. Jim has continued to pay himself the same he pays new employees, $70,000/yr.

Our math says Jim should more than double his salary! The max earnings that credit to Social Security in 2022 is $147,000. For Jim, this would be a salary increase of $77,000. At 15.3% payroll tax, this costs him $11,781 this year. However, since he does not have a fully maxed SS earnings record, this increases his monthly SS benefit by $71.88 for life. How much would it cost Jim to go out and buy a private annuity that pays $71.88 per month? One calculator² estimates $12,171. Since this payout, $12,171, is greater than the payroll tax cost today, $11,781, Jim should pay himself enough to max out his SS record this year.

Can this result be extrapolated to all owner-employees? Unfortunately, that is not the case. Since Jim is close to retirement, the actuarial value of fixed income is much higher than a year of maxed-out earnings for a 20-year-old. Below are some factors that would weigh on this very personal decision.

When an owner increases their salary:

- Older owners benefit more than younger owners.

- Owners with non-working or low-wage spouses benefit more since the spouse will take Social Security based on the owner/employee’s record.

- Owners with incomplete earnings history benefit more from additional years of salary.

- Owners with lower average historical earnings benefit more from higher-wage years.

These mathematical rules don’t include the very real behavioral benefit of “paying-as-you-go” with taxes. Owners who pay more tax today will train themselves to live on less at the same time they increase their retirement income. We are aware of the financial/actuarial benefit of fixed income in retirement, which takes the pressure off the portfolio for income generation. Equally and perhaps more important is the mental/emotional boost that comes to retirees whose income is less dependent on market returns.

This is a high-level concept with far-reaching consequences. For this reason, we avoided the inclusion of a break-even chart. In many hypotheticals we have tested, owners would benefit from paying themselves at least $74,064, which takes them to the second Social Security Bend Point³ in 2022. However, this is a topic best addressed alongside the owner’s CPA and in consideration of their circumstances. We are happy to do this for our clients anytime.

Sources

- SSA FICA Infographic https://www.ssa.gov/thirdparty/materials/pdfs/educators/What-is-FICA-Infographic-EN-05-10297.pdf

- Schwab Income Annuity Calculator https://www.schwab.com/public/schwab/investing/accounts_products/investment/annuities/income_annuity/fixed_income_annuity_calculator

- SSA Bend Points https://www.ssa.gov/oact/cola/bendpoints.html